How to improve my low CIBIL score?

How can we increase our credit score for getting a loan?

And How many credit points is this bank required to approve my loan and credit card?

These are some basic questions asked by the customer while applying for and getting rejected by the banks for any credit card or loan.

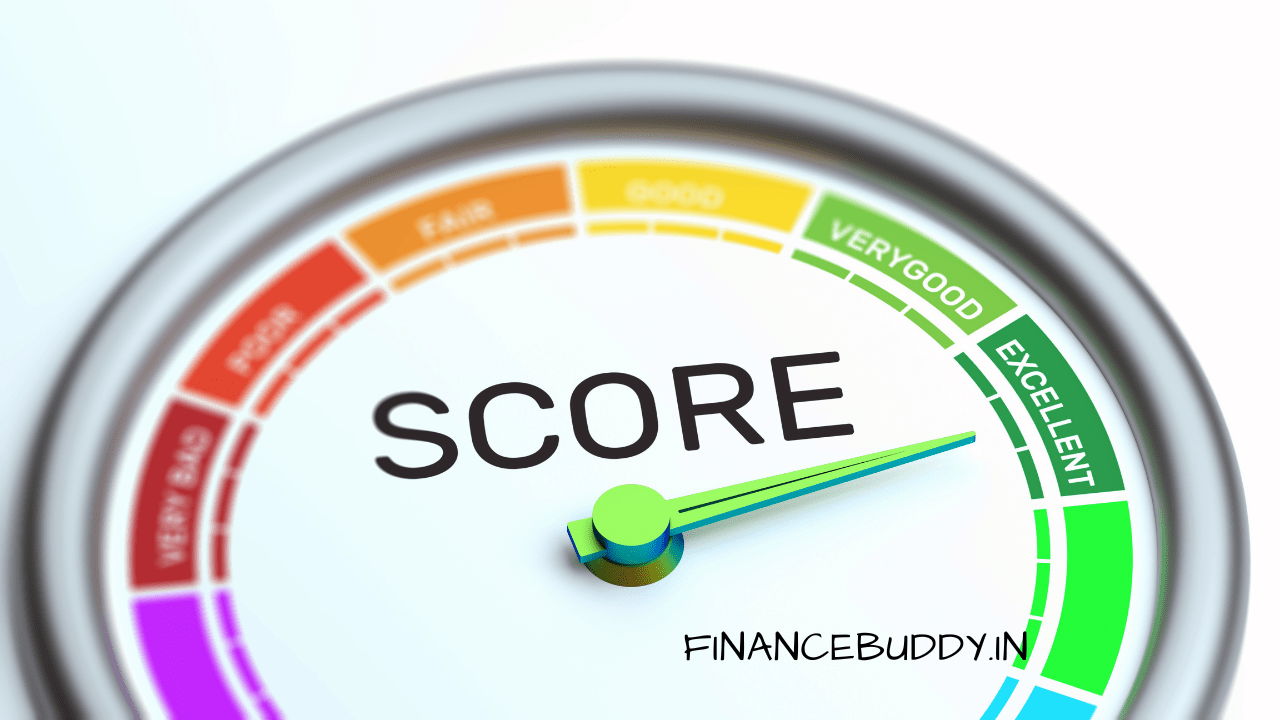

In every country, their own credit score works but most of the time, scores are found between 300 to 900.

This means 300 is the minimum score which indicates a poor rating and 900 is the maximum score which indicates excellent.

As per banking standard ratings, most of the banks required a 740+ credit score. A credit score of 750 points is fairly enough for applying any banking product.

In India TransUnion (previously known as CIBIL) maintain a database of all consumers. And they do quarterly updations in their Data.

But if you have done any mistake in the past and didn’t pay your existing dues then your credit ratings will go down to the average. And your all loan & credit card applications will be rejected by all banks.

Do you need any credit card or loan? Do you want to improve your CIBIL Score? then these few tips will help you to do this effectively.

5 Quick Tips To Improve Your Low CIBIL Score

CIBIL make 4 updates to the database every year, which are held on a quarterly basis.

So if you are also suffering from a low credit score or low average credit points then these few tips will help you to improve your ratings.

#Repay your all financial dues at the time.

Do you have any credit cards due?

Are you paying any EMI?

Have you deposited any payment cheques for paying any Bill, Loan & Credit Payments, Consumer Loan EMI, Cash Advance etc?

If your answer is yes! then you have to be more alert!

Because delays in repayments can hurt your financial ratings.

And Your credit points will be deducted due to non-maintaining financial relations properly.

Make sure you do your all repayments on time. Making all repayments on the time will improve the positive impact. Because it shows how much a person is capable of maintaining his/her financial liabilities.

#Close your spare credit cards.

How many credit cards do you have? Most people think that holding too many cards is a symbol of a rich society.

But it’s completely a misunderstanding created by the salespersons only.

According to a recent financial survey, ‘if you hold too many cards & loans then you are in big trouble or can be in the nearest future!

Because banks do a cross-check of your existing liabilities while you proceed with any application for a new Card & Loan.

All Credit Cards (including the card which you haven’t used ever) will reflect in your liability.

If your average income is below then your liabilities your application will be rejected by the bank or any financial institution.

So if you are also holding too many credit cards and using only a few of them, then you can surrender your non-used credit cards.

It will decrease your bank liability and will improve the positive impact.

#Beware of the bounces

Always remember our banking transactions play a key role to rebuild your credit score. So never give a chance credit rating agencies for reducing your score.

Keep your banking transactions clear. If you are paying any EMI then never make it late. Try to avoid paying the late fee or any extra amount by not making repayments on time.

Make sure to keep a sufficient amount in your bank account if you have issued any paycheque to someone. Because if you get any bounces in your account it will directly harm your financial ratings.

Getting regular bounces in your account will hit your credit ratings.

In the case of a Cheque, bounce bank will also charge you a penalty fee and account non-maintenance charges.

#live Away from settlements

Many customers think that after enjoying a credit card limit or using a loan amount they can go for a settlement to avoiding repay that amount.

If you also thinking the same then it’s time to stop thinking this nonsense. Because settlement, in any case, will never make you eligible for any postpay financial services like a Credit card, Loan etc.

Because while go for settlements banks will add your name to their defaulter list and will refer it to the credit bureau too.

Never try to make a settlement or be a defaulter in terms of the financial customer.

If you are unable to pay your loan and credit card amount then ask the bank to convert it into Small Amount EMI so you can pay it easily.

#Use Instant Credit Card To Improve Credit Score.

If by mistake you have lost your credit points in the past. And now you want to improve your CIBIL score then an Instant credit card or card against fixed deposits will help you to do this.

Instant credit cards are the advanced secured version of plastic money. These cards are mainly offered by the banks against your own amount.

If your credit score is very low then banks will not issue you any card or loan. But if you deposit a particular amount in any bank and ask for a credit card.

The Bank will issue a card to you and will keep your amount as security. In India, you can get 80% of your deposit amount as your card’s monthly uses limit.

Using the instant card for your daily shopping and purchasing will help you to rebuild your credit score.

Because whenever you repay your monthly bill before the billing date, Bank will reward you with a positive review.

The credit rating agency will consider these monthly or quarterly reviews as bank feedback and will improve your ratings.

These are the best tips to improve your Cibil Score without many difficulties.

If you need a loan & credit card from any bank but are unable to get it because of a low Cibil Score then these tips will help you to rebuild your credit score.

Can you explain this please…

Do u mean before Due Date or Before Bill Generation Date…

“Because whenever you repay your monthly bill before billing date, Bank will reward you with a positive review”

Hi, Ashok

I mean before the last due date. Or if you can pay it within few days after bill generation. Because while you pay your bills before last due date then it shows that you are now able to pay your credit liabilities.